This is a performance report of how the NPS invested has fared over the last 14+ years.

This is the growth of the NPS portfolio along with total investments.

My gilt-heavy NPS portfolio took a mighty tumble.

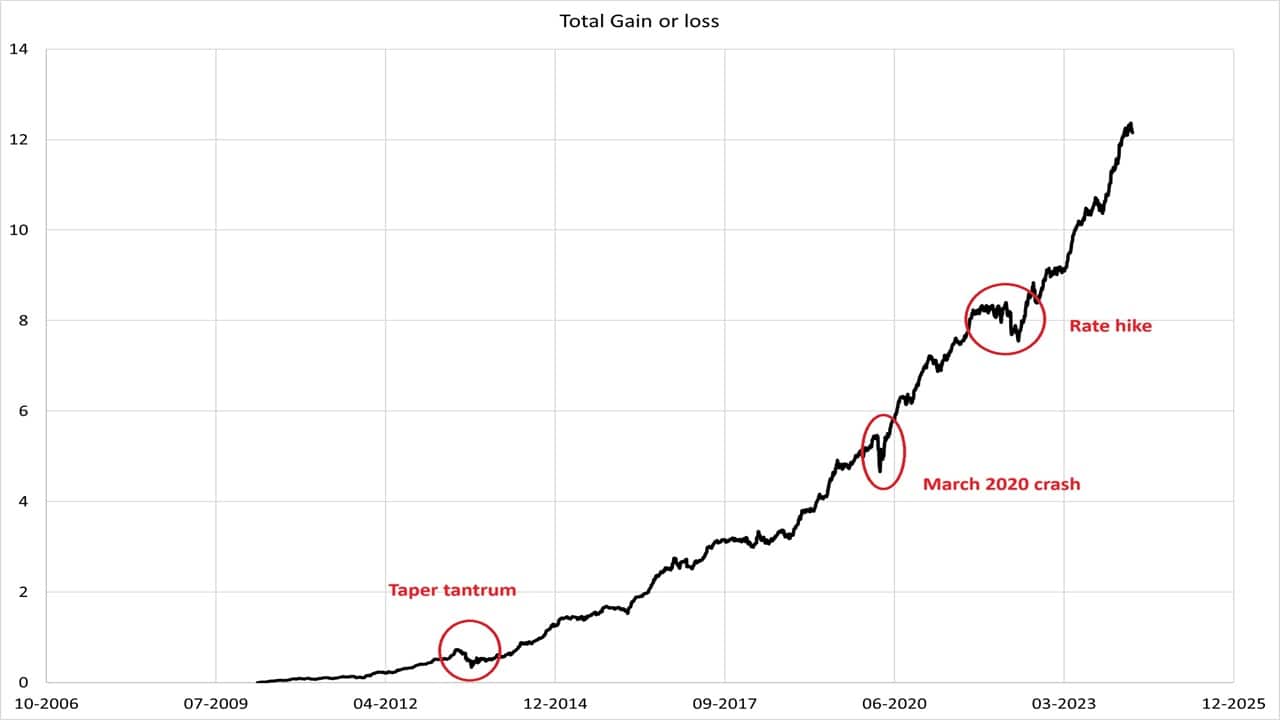

Annotated loss of gain in the NPS portfolio.

NPS vs EPFThis compares the NPS NAV (the SBI central govt fund has been used as a representative) and the EPF NAV (constructed from annual interest rate history).

I have invested in the National Pension Scheme (NPS) since 8th March 2010. This is a performance report of how the NPS invested has fared over the last 14+ years. We also compare the returns with EPF.

Note: Kindly do not assume that I am recommending NPS instruments. My situation is quite different from most. NPS is a mandatory investment for me and a full replacement for GPF. The asset allocation is 15% equity and the rest in gilts (govt bonds). If you are in a corporate setup, please recognise that NPS has a lock-in of up to 60. Most corporate employees will not work until that age. If you exit before 60, 80% of your corpus will be locked into an annuity. So, our recommendation has always been not to invest in NPS.

Also, see:

My NPS corpus is about 30.5% of my equity MF + stocks corpus tagged to retirement. It is about 20% of my total retirement portfolio. It has taken a lifetime to reduce the dependence on NPS. For more details, see Fourteen Years of Mutual Fund Investing: My Journey and Lessons Learned.

I have been part of the NPS since 2006. However, the NPS was not ready for investment then. Until then, the organisation F&A held the money with 8% annual interest. The first investment into NPS funds was made on 8th March 2010.

Join over 32,000 readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! Email * 🔥Enjoy massive discounts on our robo-advisory tool & courses! 🔥 Subscribe to get posts via email!

We shall track the progress from that date. The money was almost equally divided among the three Tier 1 (central govt) schemes offered by UTI, LIC and SBI.

With employer contribution, NPS is one of the best step-up SIPs in a mutual fund. My monthly investment today is five times more than ten years ago. That is a 14.4% year-on-year investment increase spanning two pay commissions and a promotion. You can see that in the curvature of the total investment line below.

This is the growth of the NPS portfolio along with total investments. The XIRR as of 19th April 2024 is 9.03%. Not too shabby. Before the rate hikes, it was 10%-ish.

In July 2013, the RBI increased overnight rates by 2% to stop the fall of the Rupee. My gilt-heavy NPS portfolio took a mighty tumble. This is what the NAV looked like in Oct 2013. My NPS CAGR just before the fall was 11% ish; overnight, it became 6-ish%, recovering over the next few months. When this occurred, PFRDA realised, “Aisa bhi hota hai! What if this happens just before the person retires?!” and introduced staggered withdrawals.

Annotated loss of gain in the NPS portfolio.

NPS vs EPF

This compares the NPS NAV (the SBI central govt fund has been used as a representative) and the EPF NAV (constructed from annual interest rate history).

At the time of writing, NPS has outperformed EPF, but that may not always be true! If I had invested in EPF instead of NPS ten years ago, the NAV evolution (assuming daily growth = annual interest/365) would look like this.

It is hard to beat the non-volatile growth of EPF, but it is not too shabby for a mandatory investment! The asset allocation of central govt employees can now be modified. I have not changed it (and recommend others not to do it too). Using NPS as a pure-debt fund and managing equity separately is best (see links below)

Also, see: